Tomato Newsletter No. 221 - September 2019

Your monthly resource on working capital, process optimization and issues relating to the world of corporate treasurers, IT professionals and bankers!

This newsletter is bilingual, English or German depending to the source.

Introduction:

A wonderful summer, at least in the Swiss, Austrian and Bavarian mountain regions, has come to an end. We miss spending time outside, being active and vivacious. However, the fall with its colors and festivals, the experience of nature exercising its magic, is also inspiring. And we are ready to immerse ourselves in projects and solutions that need to be implemented this year. A special time!

This month’s Catch-Up includes such topics as PSD2, logon security in IT, cyber security and more.

Remember that for any challenge related to your financial issues, ask Martin Schneider for a discussion that will clarify it. Contact Martin via email or call 044 814 2001.

- Emir: NFC- Reporting für Gruppeninterne Derivate sind befreit

- PSD2 und die Folgen im e-Banking ab Mitte September 2019

- Sicherheit in Login’s was sind 2FA und MFA?

- PSD2 with Credit Cards Payment as of 14. September

- Cybersicherheit ist ein Teil des Geschäfts

- LIBOR Phase Out by 2021: Challenge of Transition to New Index

- Swiss Tax Reform with Examples from Zurich and Zug

- Endlich - mit eBam Bankkonten Digital steuern

- Book tip: A Brief History of Humankind by Yuval Noah Harari

- Termine & Events

- From the Desk of Tomato

1. Emir: NFC- Reporting für Gruppeninterne Derivate sind befreit

Viele unserer Tomato Catch-Up News Leser zählen wir zur Gruppe der NFC-. Dem Begriff NFC- sind meist Corporates und nicht Banken zugeordnet. Dazu unsere Chart auf tomato.ch

Seit Ende Juni 2109 unterliegen gruppeninterne Derivatgeschäfte zwischen NFCs nicht mehr der Meldepflicht. Details hierzu: Klicken Sie auf das Merkblatt Ihrer bevorzugten Sprache unter dem obigen Link. Details…

Voraussetzungen:

a) Beim Corporate sind die beteiligten Vertragspartner (z.B. Treasury und Business Unit) vollkonsolidiert in derselben Gruppe.

b) Zentrales Risiko - Management innerhalb des Corporate

c) Verständigung der jeweiligen Finanzmarktaufsichtsbehörde in jenen Ländern, in denen Tochtergesellschaften, mit denen Derivatgeschäfte abgeschlossen wurden oder werden, ihren Sitz haben. Sollte die jeweilige Behörde nicht innerhalb von drei Monaten widersprechen, gilt die Befreiung als genehmigt. Deutsche Corporates informieren die BAFIN.

Lesen Sie Details: Der Treasurer, EMIR ate

Weitere Erleichterungen in Reportingpflichten mit externen Gegenparteien können folgen. Ab dem 18. Juni 2020 können NFC- Unternehmen künftig wählen, ob nur noch die Banken für das Emir-Reporting von Geschäften verantwortlich und haftbar sein sollen. Im „Der Treasurer“ sagt Adrian Obhof von d-Fine „Die Unternehmen sollten daher genau prüfen, ob es sich lohnt, ihre Meldesysteme weiter zu betreiben“.

2. PSD2 und die Folgen im e-Banking ab Mitte September 2019

DEUTSCH: Wer in der EU ab 14. September noch eine TAN von einem Zettel nutzen will, (iTAN-Verfahren), dürfte eine Überraschung erleben: Die TANs werden nicht mehr funktionieren. Hintergrund ist die Zweite Europäische Zahlungsdienstrichtlinie PSD2, die neben mehr Wettbewerb im Finanzsektor auch für mehr Sicherheit sorgen soll. TANs, auf Papierzettel sind nicht dynamisch und bis zur Abfrage zeitlich unbegrenzt gültig, sind ein grundsätzliches Sicherheitsproblem. Vor allem bei Phishing-Angriffen sind diese iTANs verwundbar.

Was ändert sich im PSD2-Raum ab 14. September im e-banking?

a) Zwei-Faktor-Authentifizierung beim Login und Online-Kartenzahlungen

b) Abschaltung der iTAN-Liste

c) Zugriff auf Zahlungsverkehrskonten bei Drittanbietern

Informationen dazu:

- ein 3:30 Minuten - Video der Deutschen Bank

- Informationen zum Lesen und Videos sind im Heise-Report eingebettet

mTAN oder sms-TAN sind gemäss PSD2 weiterhin erlaubt. Das Deutsche Bundesamt für Sicherheit in der Informationstechnik (BSI) rät allerdings von ihrer Verwendung ab.

Do you prefer English?

PSD2 (the payment service directive 2) is currently one of the most disruptive developments in banking and fintech. In effect since January 2018, it forces banks to open their customer data to third party providers. Banks typically are not in the business of competing with tech giants or start-ups, so this puts enormous pressure on them.

Watch PSD2 explained in 4 minutes presented by digitalscouting.de or

Henri Arslanian’s TED-Talk on Fintech and Banking (14 mins) distributed in October 2016. Henri Arslanian started his career as a financial markets and funds lawyer in Canada and Hong Kong,

In der Schweiz (als nicht PSD2 Raum) sind Multi-Faktor-Authentifizierung (MFA) schon länger in Betrieb. Bei e-Banking Login in der EU und USA kann man bzw. konnte man die Kontosalden mittels einfachen Logins und Passwort einsehen (2FA). Um Zahlungen auszulösen sind zusätzliche Sicherheiten nötig. Scrollen Sie weiter auf Punkt 3 und lesen Sie dazu den nachstehenden Bericht 2FA versus MFA.

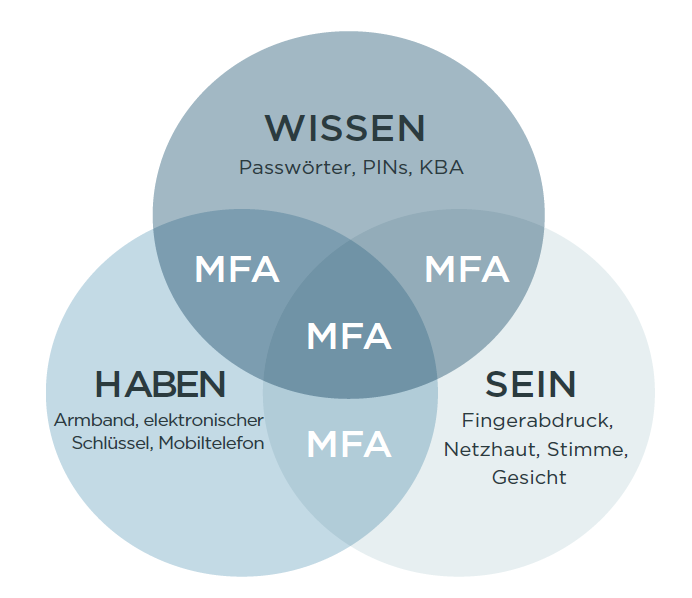

3. Sicherheit in Logins: Was sind 2FA und MFA?

Logins und Authentifizierung mit nur einem Faktor bergen erhebliche Risiken und mögen beim Online Zeitunglesen dienlich sein. Im Zahlungsverkehr im privaten e-banking oder wenn ein Corporate Mitarbeiter das e-banking nutzt sind mindestens Zwei - Faktor - Identifizierungen nötig. Das mag dem einen lästig sein. Die vielen leider erfolgreichen Missbräuche von Social - Engineering, Phishing, CEO - CFO - Fraud zeigen, dass Sicherheit unabdingbar ist.

2FA bedeutet Zwei-Faktor-Authentifizierung, MFA heisst Multi-Faktor-Authentifizierung. Der Bericht und White Paper im CIO beschreibt exzellent die Risiken und Verfahren. Durch die Kombination mehrerer Authentifizierungsfaktoren steigt auch die Gewissheit, dass der Benutzer, der gerade versucht sich zu authentifizieren, tatsächlich der ist, der er vorgibt zu sein.

Bei der MFA müssen sich Benutzer anhand von zwei oder mehr Faktoren aus unterschiedlichen Kategorien authentifizieren wie hier bebildert:

Bei der Wahl einer passenden Authentifizierungsmethode für Ihr Unternehmen sollten Sie eine Reihe von Faktoren berücksichtigen. Dazu gehören unter anderem:

- Leistungsstärke: Wie gut schützt die Lösung Ihr Unternehmen vor typischen Bedrohungen?

- IT-Kosten und -Aufwand: Was sind die Kosten pro Benutzer? Sind zusätzliche Ressourcen erforderlich?

- Benutzerfreundlichkeit: Können Benutzer die Lösung einfach und unkompliziert einführen? Können sie die Authentifizierungsmechanismen frei wählen? Bietet die Lösung ein mobiles SDK, das eine Einbettung von MFA-Funktionen in ihre eigene mobile Umgebung ermöglicht?

- Einfache Implementierung: Lässt sich die Lösung einfach implementieren und warten?

- Einhaltung von Branchenstandards: Erfüllt sie die Compliance-Standards, die Sie einhalten müssen?

- Standards: Unterstützt sie Identitätsstandards wie FIDO?

- Flexibilität: Unterstützt sie eine dynamische Step-up-Authentifizierung?

Details: Lesen Sie hier den ganzen Bericht aus dem CIO in einem PDF

4. PSD2 with Credit Cards Payment as of 14. September

DEUTSCH: Nach Einschätzung der BaFin sind die kartenausgebenden Zahlungsdienstleister in Deutschland auf die neuen Anforderungen vorbereitet. Anders sieht dies bei den Unternehmen aus, die Kreditkartenzahlungen im Internet als Zahlungsempfänger nutzen. Bei ihnen besteht nach wie vor erheblicher Anpassungsbedarf. Damit Verbraucher und Unternehmen dennoch weiterhin online mit der Kreditkarte bezahlen können, wird die BaFin für Kreditzahlungen im Internet vorübergehend nicht auf einer Starken Kundenauthentifizierung bestehen.

Die Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) wird dies zunächst nicht beanstanden. Sie will damit Störungen bei Internet-Zahlungen verhindern und einen reibungslosen Übergang auf die neuen Anforderungen der Zweiten Zahlungsdienstrichtlinie (Payment Services Directive 2 – PSD 2) ermöglichen. Details auf der BaFin Site

ENGLISH: BaFin Press release - 21 August 2019. According to BaFin estimates, card-issuing payment service providers in Germany are prepared for the new requirements. However, that's not the case for companies that use online credit card payments as recipients where significant adjustments are still necessary to meet the new requirements. To enable consumers and companies to continue using credit cards for online payments, BaFin will temporarily waive the requirements for strong customer authentication for online credit card payments. Details…

5. Cybersicherheit ist ein Teil des Geschäfts

Cybersicherheit ist heute Teil des Geschäfts – genauso als baute man einen Zaun um seine Produktionsanlagen. Die Zeit der Ausreden ist vorbei. So drückt sich Matthias Bossardt von KPMG im Interview aus.

Vor seinem Eintritt bei KPMG forschte Matthias Bossardt über Kommunikationssysteme und Cybersicherheit an der ETH Zürich und am Forschungsinstitut des Beckman Institute of Advanced Studies der University of Illinois, Urbana-Champaign.

6. LIBOR Phase Out by 2021: Challenge of Transition to New Index

In March-2019 Tomato Catch-Up, we wrote about concerns regarding Libor, which involves money, securities, foreign exchange, foreign banknotes and coins, precious metals and derivatives. Scandals over Libor (London interbank offered rates) and Euribor brought these interest rates into a shady light during the last years.

So, it comes as no surprise that the United Kingdom Financial Conduct Authority has announced it will phaseout the LIBOR by 2021, ending to the governing global borrowing index and replacing it with a new index.

On August 14, KPMG’s Jonathan Bernsen explains in a blog how the transition impacts tax and transfer pricing (TP) related documentation, agreements and systems enablement.

He explains that “the new risk-free rates that will replace LIBOR are known for all five major currencies - although the rate’s characteristics differ. Most notably, the USD (SOFR) and CHF (SARON) rates are based on the market of secured overnight funds, while GBP (SONIA), EUR (ESTER) and JPY (TONE) are based on the market of unsecured overnight funds.”

Successfully mitigating this impact requires planning and the joint effort of internal and external stakeholders. In the blog LIBOR phaseout: Mitigate transfer pricing issues, Bernson explains the LIBOR-related tax/ transfer pricing questions that are likely to pose challenges and the next steps to be taken.

- Different RFRs – impact of secured/unsecured

- Credit risk in RFR – will disappear with new system

- Term RFR – Overnight is know, what are the term rates

Details… or ask Martin Schneider via email or call 044 814 2001.

7. Swiss Tax Reform with Examples from Zurich and Zug

In the July/August Catch-Up Newsletter, we featured "Steuern Schweiz: Prinzipalgesellschaften und neue Steuersätze".

On September 1, KPMG’s Olivier Eichenberger explained how corporate taxes will look like in Canton of Zurich (in English) and KPMGs Markus Vogel for Canton Zug (in Deutsch)

New corporate taxation in the Canton of Zurich by KPMG, Key points:

- The effective income tax rate over all levels (federal, cantonal and municipal) will initially decrease to 19.70% as of 1 January 2021 (capital city, previously 21.15%). However, a further reduction of the effective income tax rate from 19.70% to 18.19% as of 1 January 2023 is planned within the framework of a new bill, which still has to go through the usual legislative process.

- Net profits from patents and similar rights will in future fall into the patent box and will thus be taxed at a maximum reduction of 90%.

- An additional deduction of 50% may be applied for expenses relating to research and development (R&D) carried out in Switzerland.

- Also introduced is the notional interest deduction (NID) which includes the granting of an imputed interest deduction on surplus equity. Surplus equity includes equity capital which, in the long term, exceeds the equity capital required for business operations. This measure is expected to be introduced only in the canton of Zurich.

Unternehmensbesteuerung im Kanton Zug von KPMGs Markus Vogel, einige Schlüsselpunkte:

- Der Effektive Gewinnsteuersatz über alle Stufen (Bund, Kanton und Gemeinde) sinkt auf 11.91% (Hauptort, bisher 14.35%).

- Der ordentliche Kapitalsteuersatz beträgt unverändert 0.0717% (Hauptort). Steuerbares Eigenkapital, das auf qualifizierende Beteiligungen, Konzernforderungen sowie qualifizierende Patente entfällt, wird zukünftig nur mit 2% in die Bemessung einbezogen.

- Mit der Einführung der Patentbox wird der Reingewinn aus Patenten und vergleichbaren Rechten mit einer maximalen Ermässigung von 90% in die Berechnung des steuerbaren Reingewinns einbezogen.

- Neu ist im Kanton Zug ein zusätzlicher Abzug für Forschungs- und Entwicklungskosten von 50% zulässig.

8. Endlich - mit eBam Bankkonten Digital steuern

Zwei grosse Institute bahnen den Weg. Eon und Deutsche Bank werden ab November 2019 alle Bankkonten zwischen Eon und Deutsche Bank öffnen, schliessen und ändern. Weitere Partner in diesem Projekt sind Swift und Omnikron. Für viele sind solche Prozesse auf der Wunschliste.

Das bedeutet für kleinere Corporates die ersten Hausaufgaben jetzt schon für später aufzubereiten. Bankkonten an die Zentrale (Treasury) bringen, Bankkonten-Prozesse zentralisieren, Bankkonten des Konzerns in einheitliche Formate zu bringen. Sich an der Swift Sprache zu orientieren.

Details lesen Sie im Der Treasurer, zusammengetragen von Desiree Backhaus

9. Book Tip: A Brief History of Humankind by Yuval Noah Harari

100,000 years ago, at least six human species inhabited the earth. Today there is just one. Us.

Homo sapiens.

How did our species succeed in the battle for dominance? Why did our foraging ancestors come together to create cities and kingdoms? How did we come to believe in gods, nations and human rights; to trust money, books and laws; and to be enslaved by bureaucracy, timetables and consumerism? And what will our world be like in the millennia to come?

In Sapiens, Yuval Noah Harari spans the whole of human history, from the very first humans to walk the earth to the radical – and sometimes devastating – breakthroughs of the Cognitive, Agricultural and Scientific Revolutions. Drawing on insights from biology, anthropology, paleontology and economics, he explores how the currents of history have shaped our human societies, the animals and plants around us, and even our personalities.

He answers such questions as:

- Have we become happier as history has unfolded?

- Can we ever free our behavior from the heritage of our ancestors?

- And what, if anything, can we do to influence the course of the centuries to come?

Sapiens challenges everything we thought we knew about being human: our thoughts, our actions, our power ... and our future.

- Mittwoch 11. Sept. 2019: Swiss Treasury Summit in Zug

- Mittwoch bis Freitag, 9.-11.Okt. 2019: Alpbacher Finanzsymposium - Kongress in Alpbach/AT

- Friday, 8. Nov. 2019: Swissquote "Conference on Artificial Intelligence in Finance" in Lausanne at the famous EFPL

- Mittwoch, Donnerstag 27. & 28.Nov..2019:

Structured Finance in Stuttgart

Enjoy your Coffee break with

Tomato Cups „Keep your Liquidity high“ !

Alle Termine unter Tomato Veranstaltungen Messen und Seminare

- 13 November 2019 at 12.00h

Swiss Finance Institute at Kunsthaus Zurich:

Credit is the engine of growth, but can excessive debt reduce the economy’s resilience to shocks?

Keynote Speakers are:- Mr. Sergio P. Ermotti, Group Chief Executive Officer, UBS Group AG

- Nobel Laureate Prof. Bengt Holmström, Professor of Economics, Massachusetts Institute of Technology (MIT)

- SFI Prof. Jean-Charles Rochet, SFI Senior Chair and Head of Research, University of Geneva and SFI

- Mr. Herbert J. Scheidt, Chairman of the Board of Directors, Bank Vontobel and Chairman of the Swiss Bankers Association

A light lunch buffet will be served after 12:00h, the conference starts at 13:00h

Details and register for the conference and for exchanging the knowledge and expertise that will keep Switzerland at the top in banking and finance. The attendance fee will be CHF 250.

We Swiss are hikers. While many of us enjoy trips abroad year-round, hiking in the mountains is in our blood and fall is an especially good time to do so. Interesting what hikes foreign publications suggest as the best hikes! That’s not where we Swiss typically go.

We have family traditions, our favorite route that’s not overrun by tourists. We combine hiking with socializing. I have fond memories about hiking. For example, I went for years with the same group of friends hiking on the Ofenpass. Over the years and all of us getting older, less frugal and less ambitious. So, each year the hikes got a bit shorter and the picnics more elaborate. Fun looking back!

The following picture dates from a weekend hiking in Valais Val d'anniviers.

Enjoy, Martin Schneider